9 Bank Marketing Strategies to Grow Deposits [Updated 2024]

Home»Blog»9 Bank Marketing Strategies to Grow Deposits [Updated 2024]

Use these proven marketing strategies to reach the right audience and increase deposit account growth.

Video Summary of This Post:

Listen To This Post:

In the aftermath of the Great Recession of 2009, community bank performance rebounded in tandem with the rest of the banking industry. By 2015, community banking institutions had returned to pre-crisis levels in terms of noncurrent loans, net charge-offs and percentage of unprofitable institutions. However, profitability has remained below pre-crisis levels in recent years.

Core deposits became stagnant over a three-year period for community banks with less than $10 billion in assets. That dormancy meant that these banking institutions’ flexibility was greatly limited, and their lending capacity was significantly reduced.

According to a recent report from CommunityBanking.org, “Nearly one-third of bankers ranked either core deposit growth or the cost of funds as their greatest challenge.” Since then a number of factors have contributed to these concerns within the Financial Services industry.

While foot traffic to branch offices had been decreasing prior to the pandemic, COVID-19 accelerated the trend. Branches will certainly continue to provide value for the foreseeable future, but physical bank locations will likely have a diminishing impact on deposit growth. Marketing professionals can find more on increasing in-person visits to your branches here.

In addition, many consumers are responding to the impact that inflation has on their financial plans. With rising costs, individuals are spending more and depositing less. It’s critical for bank marketing professionals to keep customers informed about competitive interest rates and other financial measures to help counteract the loss of purchasing power during inflationary times is critical.

Local banks and credit unions increasingly need to execute effective bank marketing strategies to reach and educate their target audiences for financial services.

This guide provides bank marketing strategies for reaching prospective customers/members in order to increase core deposits.

Modern Banking Behavior

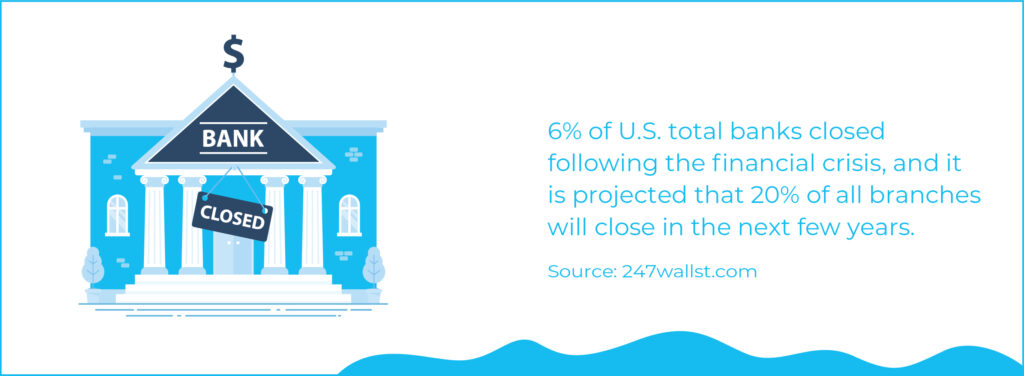

The average American’s banking behavior is very different now than it was in 2009. 6% of U.S. total banks closed following the financial crisis, and it is projected that 20% of all branches will close in the next few years. Retail branch offices have traditionally been a market advantage for local financial institutions, but the need for local bank branches to grow target markets may be dwindling. Instead, local financial institutions should invest in digital banking and mobile banking apps. At least for transactional banking purposes, many customers can’t remember the last time they walked into a physical bank. And while national banks enjoy widespread brand awareness thanks to enormous marketing budgets, awareness of community banks and credit unions in their local market is typically about half that of megabanks. This presents a major challenge for local FIs since most consumers searching for a checking account already have a brand in mind, and largely end up choosing that brand (see Oliver Wyman study). In order to attract and retain depositors, local banks must adjust how they engage customers and differentiate their brand. This includes letting customers choose how to bank–whether that means visiting a local branch or enjoying the convenience of digital banking and mobile banking apps.

As you plan a deposit growth strategy for your community bank or credit union, consider these essential tactics for increasing core deposits:

1. Local search engine optimization (SEO) ensures prospects will find you online

According to the CA Web Stress Index, 88% of consumers will shop online first before opening a checking account. You may be the closest financial institution, and you may have the best rates for your deposit accounts, but if your competitors are dominating the top organic positions in Google and Bing search results, then you are missing out on new customers. Are your prospective customers even aware of your bank?

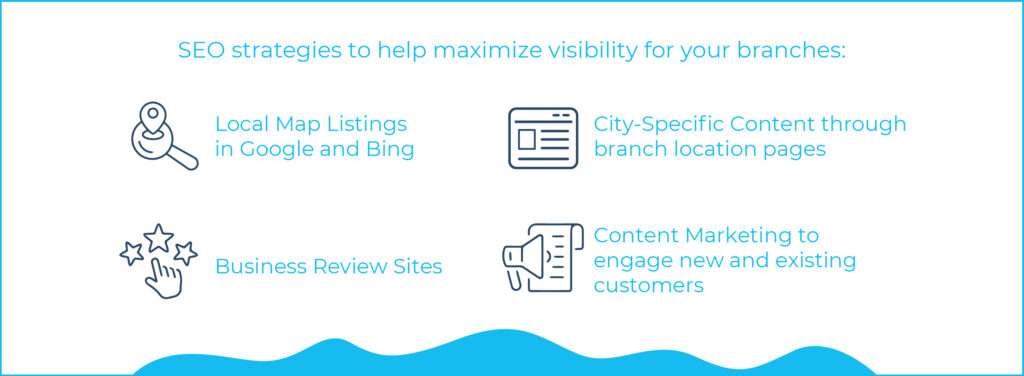

Local SEO (search engine optimization) is the key to maximizing your online visibility for each of your branches. Many elements play a role in creating a comprehensive local SEO strategy, but here are some essential strategies that you can use to get in front of your potential customers:

Local Map Listings: Create and verify online listings for each of your branches in Google, Bing, Apple, and other credible business directories. This information typically appears above organic results when a local search is performed and provides a breakdown of the essential information that your customers need most: branch address, hours of operation, phone number, a link to your website, and directions to lead them right to your door. Getting some 5-star reviews for these listings will increase your credibility, giving potential customers a greater sense of confidence that you will be able to help them.

City-Specific Content: Create pages on your website for each of your bank’s branches. Flesh them out with contact information for the branch, a high-quality image of the building, and the address. Don’t forget to add few paragraphs of unique content that describe the services you offer, your staff, etc. Insert a link to your deposits page to help drive curious visitors into confident customers. These elements work together to help each branch location page rank higher in the search engine results. More branch location page best practices here.

Business Review Sites: Whether you added your business or not, review sites like Yelp and Yellow Pages likely have details about your locations. Make sure that each of your branch locations is listed and accurate on these sites. Check each listing to ensure that your address, phone number and hours of operation are all up-to-date. Again, getting some 5-star reviews on these sites will bolster your credibility.

Content Marketing: Creating content that is valuable to your audience is an effective way to reach new prospects while providing useful resources that improve engagement with existing customers. This is an effective digital marketing strategy used by banks to promote nearly any product or service. One method is to create content that answers the questions of your customers and prospects. Take deposits for example – do your customers frequently ask you about the differences between the accounts you offer, if they should plan to keep a certain amount of money in their account, or if multiple savings accounts can help keep their savings goals on track during periods of high inflation. These topics can inspire new pieces of content that will educate your audience and open a line of communication to your community bank.

Utilizing these local SEO strategies will also make it more likely for potential customers to find you through Google searches and business review sites. Once your visitor has landed on your site or visited one of your branches, this is the time to present an attractive offer for a new deposit account.

These strategies are generally useful for increasing your online visibility to a local audience and will yield long-term results. If you’re looking to target a more specific audience, keep reading to learn more.

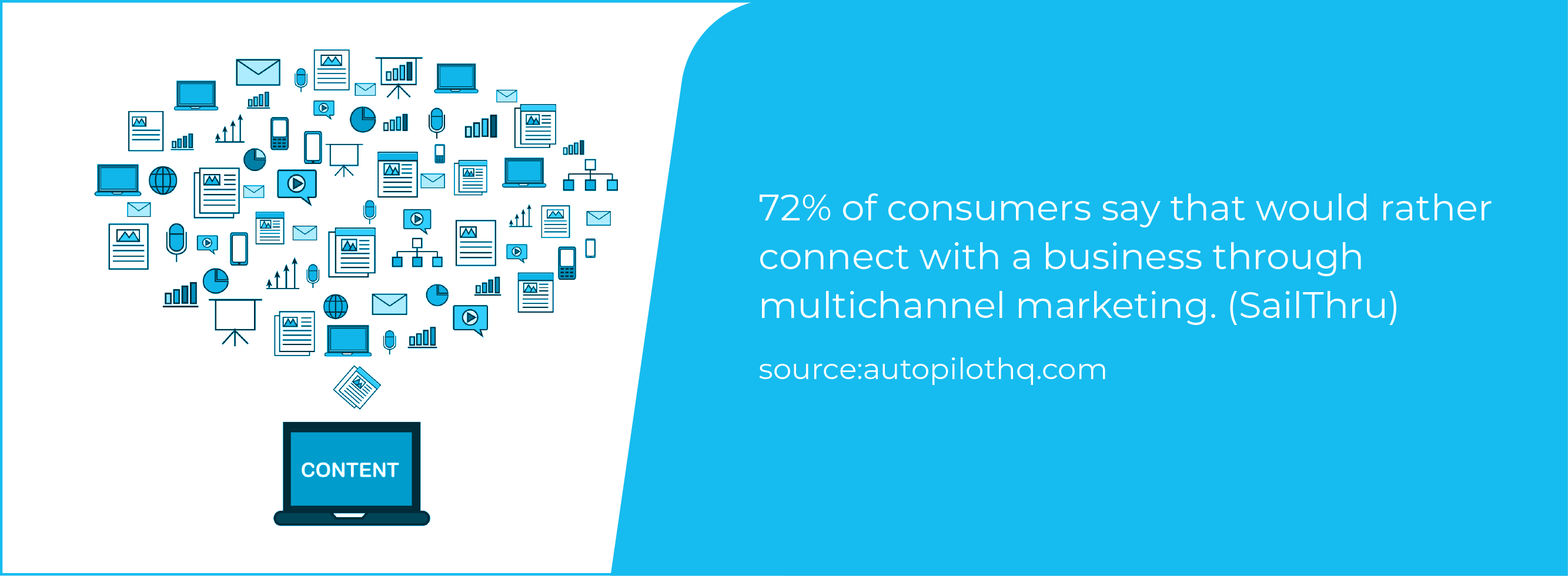

2. Use multiple marketing channels to reach your desired audience

In today’s competitive financial services climate, you can’t assume that any single channel will take your prospects through the entire buyer journey. Part of your bank marketing plan should be to identify the consumer and business personas who can significantly help you grow your deposits, then develop a multi-channel strategy, including digital channels, to reach them.

Create a profile of the type of client you wish to pursue. What is their ZIP code, for example, and what financial products would they use? Are they lifelong residents in the area, or have they just moved here from out of state? Is this their first step towards organizing their finances, or are they looking to change financial institutions after many years? Each of these groups has different needs, and present unique opportunities to open new deposit accounts. You can start by analyzing your existing deposit holders’ demographics and preferences which can help you determine their overall profitability and interest rate sensitivity. Once completed, you have the basis to design profiles that will help you attract and retain more depositors. This information will aid in designing your effective bank marketing strategy.

An important consideration as you create your desired customer profiles is to research what you think may be attractive to your audience. Millennials, Gen Z, and younger audiences can engage with financial services differently; understanding these nuances can help improve the relevance of your products and communications (check out our contribution to this podcast about attracting millenial and gen z customers to your community bank). However, when it comes to growing deposits, don’t forget that Baby Boomers still hold two-thirds of all deposits, with substantially more assets under management at RIA (registered investment advisory) firms. The most effective bank marketing strategy will target multiple generations.

Once you know who you want to reach, integrated marketing strategies that include multiple touch points from direct mail, video, website content, email, print, and digital channels can help you grow deposits from existing customers and convert new customers to boost your bank’s deposits.

3. Use paid search marketing to your advantage

It’s become the norm for potential customers to turn to a search engine to research a product or service before they make a decision. Even the majority of people who decide to open an account at a physical branch gather information online first. As a result, it’s become essential to your marketing efforts to place your community bank in front of these searchers. This much is obvious, but many financial institutions aren’t leveraging the full potential of their online presence with an effective search marketing campaign.

By utilizing strategies like pay-per-click (PPC) advertising using tools like Google Ads, community banks have the opportunity to push past their competitors and gain prominence at the top of the search engine results pages. Paid search campaigns are so effective because they can specific to your target audience according to the exact phrases they are searching Google for. This is accomplished using target keyword groupings, specific ad content, geo-targeting and a host of other options.

Paid search advertising offers a clear path to presenting your services out to a highly-qualified target audience. Here are some things you should consider when building a paid search campaign if your goal is to increase deposits:

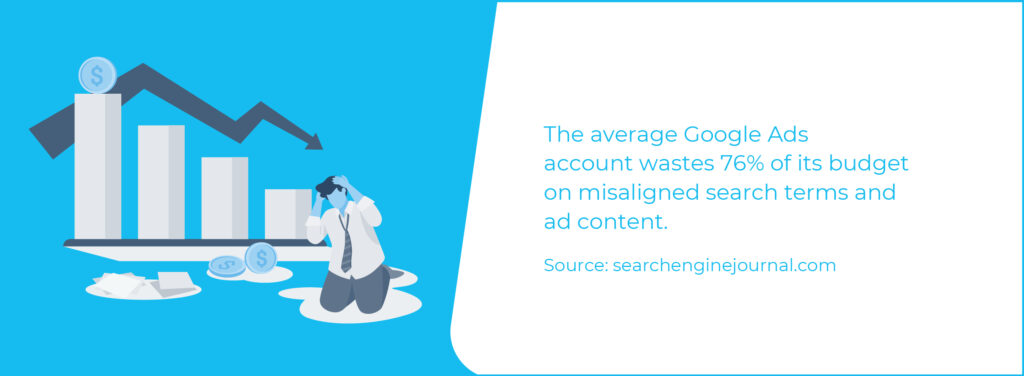

Build ads for each deposit account: Create ads that focus on individual deposit services and choose target keywords that will deliver those ads for relevant searches. Your ads should always align with the keywords you’re targeting. For example, if someone searches for “open savings account near me” then you’ll want to show ads related to your checking options, rates, etc. If ads for your premier checking accounts are displaying from a search related to CDs, then there’s little chance that users will actually click on them. This is a typical mistake by many search advertisers; in fact, the average Google Ads account wastes 76% of its budgeton misaligned search terms and ad content.

Use thoughtful geo-targeting: Specific targeting is key to driving qualified traffic and conversions. If your targeting area is too broad, then you may wind up with a rapidly-diminishing budget that is wasted by users who aren’t part of your target audience. If you have multiple branches, it’s smart to target prospects within a small radius around each of your locations.

Consider your competition: Keeping a watchful eye on your competitors is a standard practice in search marketing efforts. If you see ads for your local competitors in the search engines, take a look at the types of deposit accounts they’re promoting and how they differentiate. This can help you get an idea of what their customers are interested in, and how they’re addressing those interests. You can also target your ads to appear when someone performs a search for one of your competitors, giving you the opportunity to position your bank as a better solution to their needs. You’ll never outspend a megabank, but you can absolutely target megabank prospects or existing customers to help them understand the benefits of banking locally.

The world of PPC is vast, and there are many elements that we haven’t touched on in this article – budget, ad extensions, display advertising, remarketing/retargeting, customer-match, and more. If you plan to enhance your online presence with paid ads, your best bet is to partner with a digital marketing agency that is experienced in helping banks grow.

4. Leverage social advertising to target prospects and existing customers

Many financial products are designed to assist people throughout the various stages of their lives – higher education, relocation, purchasing a home, starting a family. Social advertising – the use of ads on social media platforms like Facebook and LinkedIn – is a marketing strategy that enables marketing experts to target these individuals with ads that address their changing lifestyles and countless other demographics or behaviors.

Social media platforms offer powerful targeting tools that allow you to deliver highly-focused ads to a specific audience based on their interests and lifestyles. Couple this social reach with a comprehensive understanding of your audience, and you can create social media ads that drive highly-qualified traffic to your site. For example, a LinkedIn Ads campaign promoting business IOLTA checking accounts can be delivered to business owners of law firms with less than 50 employees within your target geographic markets.

This targeting also allows you to maximize social reach by creating ads tailored to the needs of your specific audiences. This makes the most of your ad spend by only showing your ads to individuals that you’ve selected through targeting. You can further narrow your marketing strategy to target a specific list of customer email addresses (e.g. loan customers who don’t also have a checking account with your financial institution). By tapping into these audiences and following social advertising best practices, bank marketing experts have the ability to reach highly qualified prospects (and existing customers/members) with timely and relevant offers. Find related resources on our blog about Facebook Ads best practices and LinkedIn marketing for bankers.

5. Create a unique digital banking presence

As we head into 2025, few things are certain. However, you can count on your customers and prospects spending more time on their mobile phones than ever. Your digital banking experience is now a big part of how users perceive your financial brand. For digital banks, the digital banking experience IS the brand.

A study by Forrester found just 36% of US banking customers think their primary bank’s app offers unique value that’s different from others. Offering a feature rich app with relevant personal financial management (PFM) tools, actionable insights, and useful integrations is a compelling win theme for deposit acquisition.

6. Deliver customer service that is both friendly and educational

There was a time when serving up a smile and a small gift was enough to gain new accounts. Now your community bank is competing against larger banks as well as online-only financial institutions for customer loyalty. That means you need to do your research, then roll out the red carpet. Identify the customers your bank would like to attract and try to understand their banking lives.

For example, busy people may not want to go through the hassle of switching their checking account, so you may not want to lead with checking account marketing strategies (more ideas in our bank switcher marketing guide). However, a competitive loan offer may entice the same personal or business customer. Once you establish engagement with this one product, it’s easier to cross-sell other products such as that no-fee checking.

On that note, make teller outreach a core part of your internal marketing strategy. In the era of direct deposit and mobile banking, customers don’t have to visit a physical branch. When they do, make it count with a friendly, personalized customer experience. This is often what distinguishes a community bank from larger, more impersonal institutions. As the teller processes the customer’s transaction, they can recommend products that would be a good fit, such as higher yield savings products or investment services.

When it comes to high net-worth customers, pick up the phone and get personal. Relationships are everything and individuals and businesses will appreciate the special touch and attention to their needs and satisfaction.

Overall, don’t take customer loyalty for granted. Remember you’re not the only bank trying to woo potential customers or sell additional products to existing customers. Win their engagement by being genuine, accessible, thorough, and proactive.

7. Tell a (good) story

Effective storytelling can yield serious results. Research backs up common-sense that people purchase more often from companies that engage them with education. Invest in relevant educational content by creating high-quality website content and blog articles that will inform your audience.

Draw inspiration for these articles from common questions you receive on a regular basis, or highlight services that would be most beneficial for your target audiences. If you’re trying to sell a particular product – deposit accounts, for example – use your content as an opportunity to sell your audience by educating them about that product. By doing this, you’re creating an effective resource for your audience while simultaneously showing them why your services are the solution for their needs. Don’t forget to take advantage of client success stories- testimonials make for great storytelling!

Your target customers are more likely to respond to a local bank that actively works to strengthen its community. Your fortunes are intertwined with those of your neighbors and that is a powerful selling point.

8. Promoting ICS-Based CDAR Options

In the wake of recent bank failures, promoting your financial institution’s participation in ICS®, the IntraFi Cash Service®, and CDARS® can help you attract risk-averse customers and increase overall deposit value. Target both current and prospective customers with the promise of accessing millions in FDIC insurance through demand deposit market accounts, money market accounts, and CDs. Our top three marketing tips for promoting the IntraFi Cash Service are:

Email and Social Media Marketing: Create emails and social posts to drive awareness about your financial institution’s ICS-based CDAR options to your current customer base. This can help reach people who may need the service now or will in the future.

Paid Advertising: Target new customers who are searching for demand deposit market accounts, money market accounts, large deposits, or handling cash reserves. You can also use retargeting to reach prospects who viewed your previous ads or deposit account pages.

SEO: Optimize your bank website to target local customers who are searching for CDARS or similar services. Organic results are better trusted and receive more clicks.

9. Remove Account Opening Friction & Fraud

Both consumers and businesses increasingly prefer to open deposit accounts online, but they have expectations. Does your bank’s digital account opening experience offer the following?

Mobile-first, intuitive design.

Ability to fund an account with a debit card, credit card, or direct transfer from another financial institution.

Ability to remove identification and facial recognition from the application.

Ability to complete the application in less than 5 minutes.

Automated identity decisioning to mitigate complex fraud.

Single platform that applicants, in-branch employees, and your call center can all work from.

Email automation to help applicants return to an incomplete application.

Simply launching digital account opening does not guarantee success. It’s critical to invest in online account opening software that will delight your applicants with a frictionless user experience while tirelessly combating fraud.

Take the next step to increase deposit growth today

Which of these bank deposit marketing strategies will you use next? With a proactive plan that capitalizes on your institution’s existing strengths, your FI can create winning strategies to increase deposits and thrive in a new era banking.

Now that you’ve discovered how to grow bank deposits, do you need a partner that can execute your deposit growth strategy? BankBound works exclusively with community banks and credit unions, using data-driven marketing to ensure the best ROI. Reach out to start a conversation, we’re always happy to talk financial marketing!

Do you have additional marketing ideas for growing deposits? Let us know and we’ll add them to this post!

{BONUS} 30 Additional Deposit Gathering Strategies to Grow Your Bank:

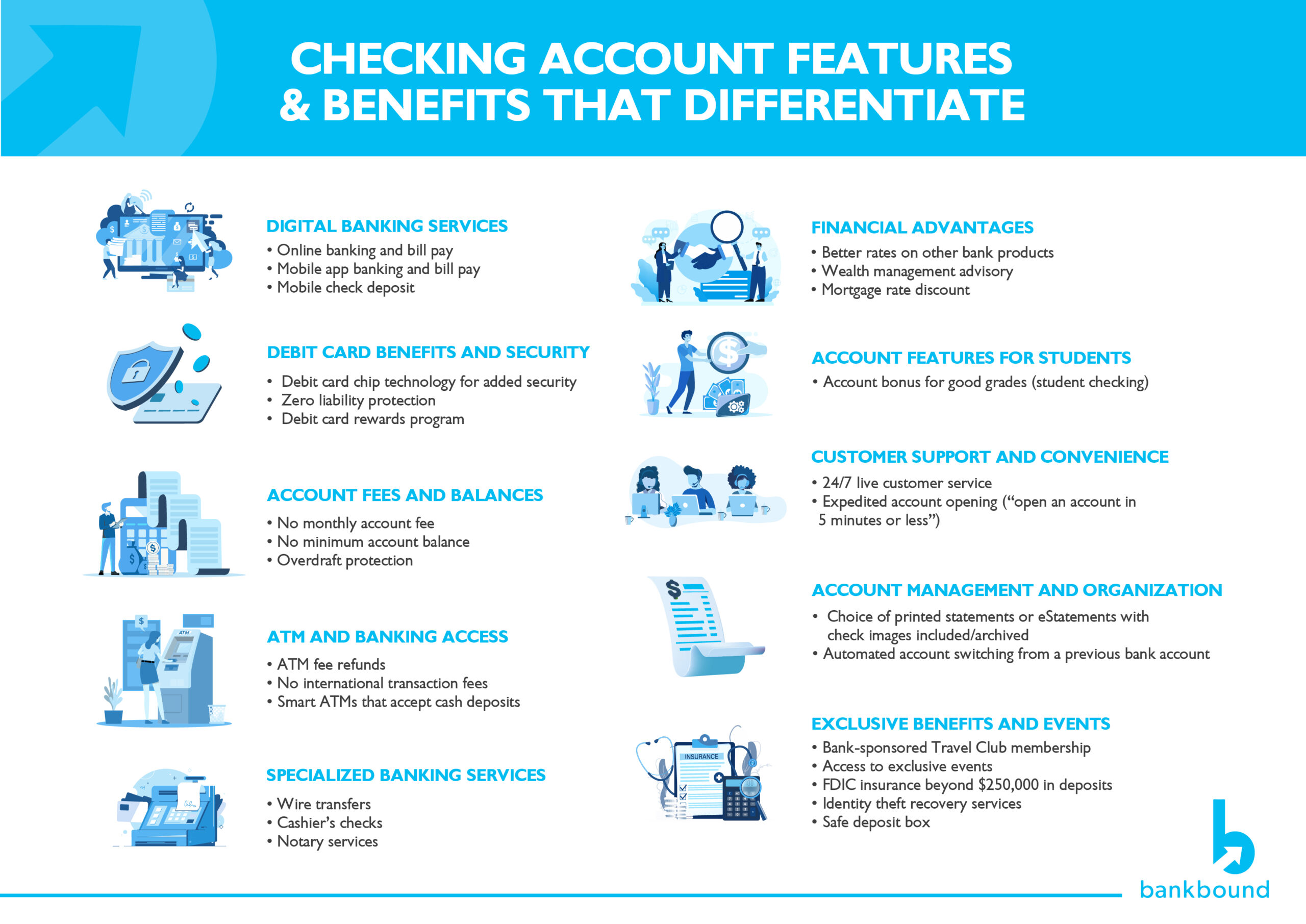

Free gifts for opening a checking account (new toaster anyone?)

Cash incentives to open a new account (We’ve seen offers as high as $600, but cash incentives often require a certain amount of direct deposits within 60-90 days (typically $500+), a certain number of transactions completed (typically 5-10), and sometimes a savings account must also be opened and funded)

Tiered rates based on higher deposit balances

Referral incentives for signing up friends

Internal employee competitions

Offering completely free checking to earn new customers, with an intentional up-selling strategy

Offering relevant checking accounts for specific life-stages (e.g. kids checking, youth/teen checking, student checking, 55+ checking)

Offering high-interest checking products

Offering a checking account that provides a higher interest rate based on how long the account has been open

Lending discounts when loans are setup with an auto-pay checking account at your bank

Offering personal financial management tools for deposit customers (or a cash management solution for commercial deposit customers) that make your financial institution especially sticky, increase share of wallet, and gain valuable intelligence on customers

Manually calling customers with other products who don’t have a checking account or other product with your bank

Manually calling on customers before their CD matures or special rate period ends (consider giving them a rate increase for renewing their CD for another term – more CD marketing strategies here)

Offer other benefits like cyber-security as part of account ownership

Become the official bank of a local college/university

Advertise on rate comparison websites (e.g. bankrate.com, nerdwallet.com, depositaccounts.com, etc.)

Use marketing automation to nurture prospects that are not quite ready to make a decision

Participate in reciprocal deposits (which are no longer considered brokered deposits thanks to the Economic Growth, Regulatory Relief, and Consumer Protection Act)

Partner with a local travel agency to create a customer Travel Club that offers discounted trips but requires members to have an active account with your bank

Partner with social media influencers and niche publishers to increase visibility with new audiences

Early direct deposit (many FIs now offering the ability to get paid 2 days early)

Custom debit card design

Automatic sweeps into higher interest accounts

Overdraft protection

Safe deposit box

FDIC insurance beyond $250,000 in deposits via ICS/CDARS

Added mobile app security (fingerprint or two-factor authentication)

Monitoring/alerts of recurring subscription payments

Choice of printed statements or eStatements with check images included/archived, and optimized to include marketing offerings, financial insights, or other useful information

Debit card rewards program

24/7 live customer service

Smart ATMs that accept cash deposits, are contactless, mobile-friendly, have a video teller (ITM), or integrate directly into your banking core